Regulator seeks power to discipline errant insurance cos

- Update Time : Saturday, February 8, 2025

TDS Desk:

Insurance regulator now wants requisite power to adequately punish errant insurers for bringing them under control in the wake of widespread allegations of noncompliance, especially non-settlement of huge claims of policyholders.

To this end, the Insurance Development and Regulatory Authority (IDRA) will soon send a proposal to the government for amendment of the Insurance Act 2010, officials have said.

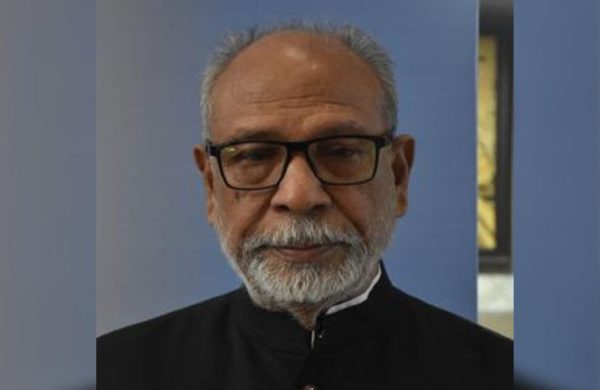

They say the interim government appointed Dr M Aslam Alam chairman of the IDRA in September last following the August regime change. Recently, the Financial Institutions Division (FID) under the Ministry of Finance instructed Authority to expedite efforts to lessen the number of unsettled insurance claims.

However, the IDRA chairman informed a recent meeting at the FID that the regulator lacked necessary power under the current insurance law to take actions against errant insurers.

Contacted, FID secretary Nazma Mobarek recently the IDRA chairman informed her about the lack of authority to enforce orderliness in the insurance sector.

“We have asked IDRA to send proposal for making necessary amendment to the insurance act to empower the regulator,” she said.

At the end of September quarter, some Tk 33.90 billion worth of claims remained unsettled in life-insurance sector while in non-life sector the unsettled-claim amount stands at Tk 28.25 billion. In the non-life-insurance sector, some 16,664 claims piled up.

Officials say the regulator receives scores of complaints regarding non-payment of claims everyday and forwards to the companies concerned for taking necessary steps. However, the insurance companies hardly pay any heed to regulator’s instructions

The IDRA chairman, Dr M Aslam Alam, recently that problems in life- insurance sector reached an “intolerable level” as thousands of insured are not getting their claimed funds. Many companies are not paying them the money for years.

He said some people blame the IDRA for not giving required attention to resolving the insurance-sector problems. “Maybe, it is true to some extent but not as a whole.”

“But, legally IDRA has some limitations. In many cases it was found that the insurance companies did not obey IDRA’s intervention. We could not force them to follow our intervention,” he said.

Mr Alam mentioned that his predecessor had been forced to resign by people of only one insurance company.

“Many insurers take the advantage of legal loopholes, which is not in favour of interest of the insured,” he said.

He said first and second years’ premiums of insurance policy are “lucrative” for insurance agents as they can keep as high as 90 per cent as agency cost. From the third year, according to the rules, the agency commission goes down drastically and so they feel discouraged from continuing the policy and give efforts to get new policies to get higher commission.

“Due to this provision thousands of policies lapse before reaching the third year,” he said about the insurance imbroglio, adding: “Now we plan to lower the initial years’ commission and introduce a flat rate for the entire policy tenure so that the agents engage similar efforts throughout the policy lifetime.”

Mr Alam said in the case of one violation of rules for one particular incident, the IDRA can penalise up to Tk 0.5 million.

“In some cases, it was found that some insurers had made millions of taka through violation of rules but we could not penalise them more than Tk 0.5 million,” he said.

The errant insurers are happy to pay the tiny amount as they can legalise the unlawfully- earned millions this way, he notes. “Insurers are thus not afraid of our actions as the penalty is very small.”

Mr Alam said the watchdog has the capacity to cancel licence of an insurer but that is “very extreme intervention” where many things are related. Fate of thousands of employees, insurance policyholders, and financial issues is involved with this.

He said taking IDRA’s approval is necessary to appoint chief executive officer and adviser in an insurance company. However, if it raises objections for any particular person for such post, they appoint them as consultant. “We want to make IDRA’s approval mandatory for appointment to any senior management post.”

Many companies even do not make payment against fines imposed on them, as seen by the new chief of the regulator.

In case of massive violations, the IDRA can suspend the board of directors and appoint an administrator but cannot dissolve or recast the board. Running a big financial company through one administrator may result in massive irregularities. “IDRA should have power to dissolve board and appoint an interim board in the errant companies.”

Mr Alam thinks that the IDRA should have power like another regulator, the central bank, in matters like shareholding and directorship by one family, appointment of directors, independent directors, appointment of CEO with suitable educational backgrounds, and appointment of deputy managing directors and additional managing directors.

The IDRA now plans to make ‘diploma in insurance’ mandatory to get appointed in senior management.

Also, he said, the Authority has no rule-making authority which the central bank and the Securities and Exchange Commission have. It needs to go to the government for preparing any rules or regulations, which is a big impediment. “Even if we want a small amendment, we need to wait at least a year.”

He goes on listing the must-haves: “We want such a legal reform that can help make IDRA effective and resolve the longstanding problems in insurance sector.”

Contacted, Nasir Uddin Ahmed (Pavel), president, Bangladesh Insurance Association (BIA), told the FE Friday that the insurance act had not been amended for long.

“The government can amend insurance act for the greater good of the sector, but holding prior consultations with the stakeholders before that will make it more effective,” he said.

Mr Pavel feels that not only the provision of penalty, there are many other areas where changes can be brought.

Editor & Publisher: Golam Mostafa Jibon

News & Commercial Office:

2 R. K Mission Road, Dhaka & Railgate, Sirajganj.

Hotline: 01715-319996, 01558-314179

E-mail : editor.thedailysky@gmail.com

news.thedailysky@gmail.com