Why some banks are flooded with cash flow when most face shortages

- Update Time : Saturday, November 16, 2024

TDS Desk

While some banks have been struggling to survive due to severe liquidity shortages, well-reputed banks have seen a significant increase in cash flow, thanks to high deposit collections and low investment levels.

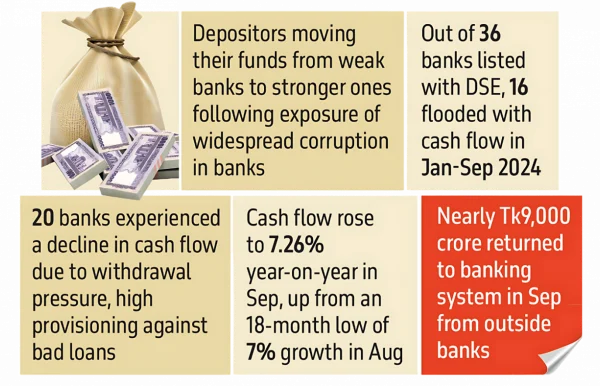

This shift is largely due to depositors moving their funds from weak banks to stronger ones, following the exposure of widespread corruption in banks controlled by the S Alam Group and other politically influential figures in the two months since the regime change on 5 August.

Out of 36 banks listed with the Dhaka Stock Exchange (DSE), 16 were flooded with cash flow in January-September 2024, thanks to high deposit inflows, while 20 other banks experienced a decline in cash flow due to withdrawal pressure and high provisioning against bad loans caused by corruption during Hasina’s 15-year regime.

For instance, the net operating cash flow per share (NOCFPS) of BRAC Bank, one of the largest private commercial banks, doubled to Tk49.51 for January-September 2024, compared to Tk25.10 in the same period last year, according to its disclosure posted on the DSE website.

Explaining the reason, the bank said cash flow increased significantly mainly due to higher deposit mobilisation from customers, the bank’s borrowing, and the growth in the loan portfolio being lower compared to the same period of the previous year.

NOCFPS of City Bank increased to Tk42.38 during the same period, overcoming a negative cash flow of Tk5.20 in the previous year. Mutual Trust Bank experienced its NOCFPS double to Tk44.27 from Tk22.42 during the same period.

The significant rise in cash flow was due to high deposit collection and low investment, according to their disclosures.

The rise in cash flow is also evident in overall deposit growth in the banking industry, which increased to 7.26% year-on-year in September, up from an 18-month low of 7% growth in August, according to central bank data.

Deposit growth increased as nearly Tk9,000 crore returned to the banking system in September from outside banks, with depositors returning their money to good banks.

Loan demand is very low as businesses have not been expanding amid political uncertainty, said a senior executive of a private commercial bank.

As a result, banks with good reputations experienced an increase in cash flow due to high deposit collection, the banker said.

High deposit growth also eased pressure in the money market, pushing the call money rate down to the central bank rate.

Interest rates in the call money market are now below the policy rate, which reflects that money rates have returned to a normal trend.

Usually, the policy rate is supposed to be higher than the call money rate, but the trend was the opposite for the past few years due to an ineffective monetary policy framework.

As a result, banks were borrowing from the central bank at cheaper rates, making the call money market dysfunctional.

However, the Bangladesh Bank implemented an interest rate-targeting-based monetary policy from June last year. Moreover, the central bank stopped providing liquidity support to banks by printing money from August.

At the same time, it gradually increased the policy rate, which reached 10%. As the central bank stopped providing liquidity support, banks are now borrowing from the call money market.

Low investment demand and high deposit collection have brought the call money rate down to below the policy rate after a long break.

The Bangladesh Bank introduced a guarantee mechanism to allow weak banks to borrow money from other banks instead of the central bank.

This resulted in weak banks borrowing from other banks under the central bank’s guarantee scheme, which has also helped to make inter-bank transactions operational.

WHICH BANKS LOSING DEPOSITS

Dozens of banks controlled by politically influential people are in negative cash flow due to massive corruption.

For instance, 10 banks – eight of which are Islamic banks controlled by the S Alam Group, IFIC Bank controlled by former private sector adviser to the then prime minister Salman F Rahman, and UCB controlled by former land minister Saifuzzaman Chowdhury – have all reported negative cash flow.

In August, the Bangladesh Bank dissolved the boards of nine banks that were looted by the S Alam Group, Salman F Rahman, and Saifuzzaman Chowdhury.

Those banks have been facing severe deposit withdrawal pressure after massive corruption came to light since the regime change.

The Bangladesh Bank also exposed the real health of these banks, which had been hidden by taking undue liquidity support from the central bank during the Hasina regime.

Islami Bank, once one of the largest deposit-taking banks in the country, is now facing negative cash flow due to intense deposit withdrawal pressure.

Once regarded as one the country’s best banks, its fortunes declined after it was taken over by the S Alam Group in 2017, amid widespread corruption following the regime change.

The Bangladesh Bank dissolved the board in August to protect depositors’ money, which slowed down withdrawal pressure.

The NOCFPS of Islami Bank was negative Tk3.02 for January-September 2024, compared to negative Tk48.09 for January-September 2023.

The improvement in cash flow was mainly due to an increase in placements from other banks (Tk7,374 crore) with the intermediation of the Bangladesh Bank under its guarantee introduced in August.

The increase in total provision against investments compared to the previous period is blamed for negative cash flow, according to its disclosure posted on the DSE website.

Negative cash flow occurs when a bank spends more than what it receives, but this need not always indicate a loss.

For example, payments may be due before receiving income, and the bank may spend more than it has at that time, leading to a cash flow problem.

If a bank continues to lose money, it may have to lay off employees, forgo pay cheques, fall behind on payments to vendors and creditors, or even shut down.

Social Islami Bank, another S Alam Group-controlled bank, recorded a negative NOCFPS of Tk37.56 for January-September 2024, compared to Tk2.63 in the same period last year.

The NOCFPS decreased due to higher cash outflow in respect of deposits and investments, the bank said in its disclosure.

Former land minister-controlled UCB recorded a negative NOCFPS of Tk6.79 for January-September 2024, compared to a positive Tk33.24 in the same period of the previous year.

The NOCFPS of Salman F Rahman-controlled IFIC Bank turned negative at Tk2.42 from a positive Tk3 during the same period.

Editor & Publisher: Golam Mostafa Jibon

News & Commercial Office:

Railgate, Sirajganj & 2 R. K Mission Road, Dhaka.

Hotline: 01715-319996, 01558-314179

E-mail : [email protected]